Platform Overview

Platform Overview

Unified Intelligence

Unified Intelligence

Customer Engagement

Customer Engagement

Commerce and Fulfillment

Commerce and Fulfillment

About Us

About Us

Come Work with Us

Come Work with Us

Newsroom

Newsroom

Events

Events

Insights

Insights

Blog

Blog

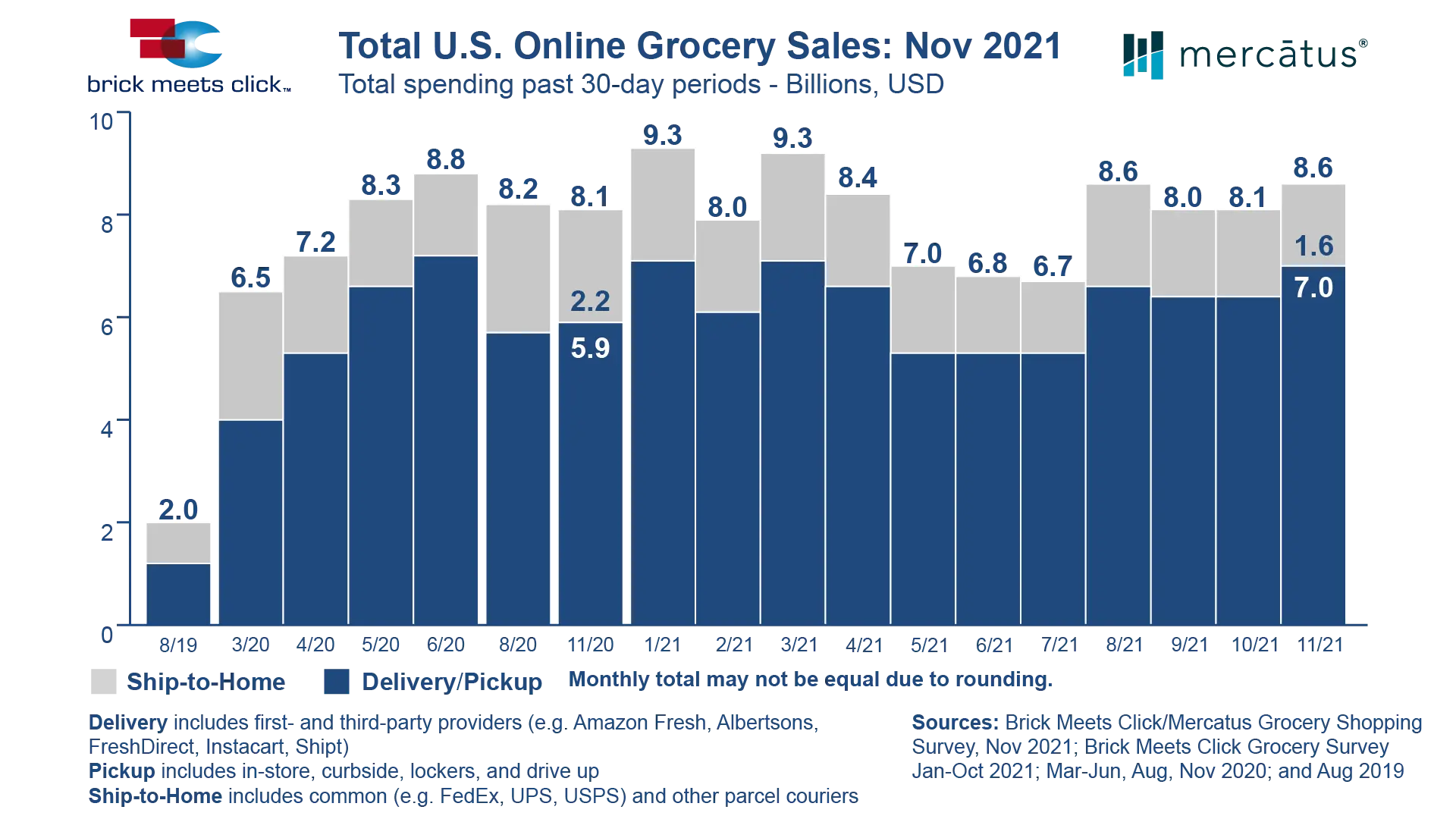

Total U.S. Online Grocery Sales for July 2021 Down 2% Month over Month

Barrington, Ill. – Aug. 23, 2021 – The U.S. online grocery market generated $6.7 billion in sales during July, as ship-to-home sales declined to $1.4 billion while the combined pickup/delivery segment remained steady at $5.3 billion for the third straight month, according to the Brick Meets Click/Mercatus Grocery Shopping Survey fielded July 29-30, 2021. The overall sales decline of 2% was driven largely by an 8% drop in ship-to-home sales versus June, while pickup/delivery sales have stabilized. Sales levels for pickup/delivery and ship-to-home are respectively 4.5 and 1.8 times greater than pre-COVID sales in Aug. 2019.

“The July results clearly reinforce that online shopping has maintained a significant portion of last year’s gains, especially for pickup and delivery, but the surge in new COVID-19 cases during July appears to have impacted shoppers’ buying behaviors differently than at the onset of this crisis in 2020,” said David Bishop, partner, Brick Meets Click.

The ongoing independent research initiative, created and conducted by Brick Meets Click and sponsored by Mercatus, showed that July’s overall sales decline was caused by a decrease in spending per order and a slight drop in monthly order frequency, which were partially offset by an increase in the number of monthly active users (MAU).

The weighted average spending per order across all three receiving methods shrank more than 5% in July 2021 versus a month ago due to two factors. First, the ship-to-home average order value (AOV) was nearly 19% lower versus June 2021, while the pickup/delivery AOV essentially held steady. Second, ship-to-home captured a larger share of orders on a month-over-month basis, which contributed further downward pressure on the top-line AOV because ship-to-home’s spending per order is typically about half that of pickup and delivery orders.

Order frequency dipped slightly, just under 1%, to 2.68 orders per monthly active user during July 2021 as compared to 2.70 during the prior month. Ship-to-home grew its share of monthly online grocery orders by nearly three percentage points in July to 34%. Although this resulted in a share loss for the pickup and delivery segment overall, delivery performed well, while pickup lost five share points on a month-over-month basis. Notably, more than four in 10 MAUs have placed three or more orders per month since Jan. 2021, stabilizing after COVID peak levels in 2020.

The number of U.S. households that bought groceries online in July, using any of the three receiving methods, jumped nearly 5% to 66.5 million households compared to June 2021. This gain reflects increases across all age groups with the youngest (18-29 years old) climbing the fastest by more than 7%. Somewhat surprisingly, the share of the MAUs who received an order via pickup dropped three percentage points on a month-over-month basis, while delivery and ship-to-home grew by six points and four points respectively.

“Although pickup continued to have the largest MAU base, share of orders, and sales during July 2021, concerns about the Delta variant’s transmissibility may be motivating customers to temporarily shift away from pickup as a means of social distancing,” Bishop explained. “Even though many retailers have implemented ‘contactless’ tactics since last year, pickup in the U.S. still often involves some degree of human contact, such as when an employee puts the order in the customer’s vehicle. So, for some, choosing delivery feels like a better, safer option as we navigate this next wave of COVID.”

July’s repeat intent rate, which measures the likelihood that a MAU will order again in the next month with the same grocery service, dropped to 56%, down four points compared to a month ago. The month-over-month decline was largely the result of a greater than four-point dip in the more-frequent customer segment’s intent rate as the first-time customer segment was down less than one point. And, while customer satisfaction with the services operated by grocers continued to trail those of mass/discounters relative to intent rates, the gap between grocers and mass/discounters shrank nearly 50% to just over four points in July versus June 2021.

The share of online customers who used both a grocery service and a mass/discount service to buy groceries during July 2021 contracted to 25%, down about three percentage points versus the prior month. This downtick was attributed to fewer grocery customers shopping with mass/discount retailers other than Target or Walmart, as cross shopping with both these two retailers increased between the June and July months.

“Grocers should be thinking about near-term improvements that will set them up for ongoing success as the monthly results reinforce that the online customer wants flexibility and convenience,” said Sylvain Perrier, president and CEO, Mercatus. “Progressive retailers are reducing operational sources of friction, like the frustration and uncertainty associated with wait times. At the same time, grocers need to better understand their core customer so they can build more meaningful engagement that leads to increased share of wallet.”

About this consumer research

The Brick Meets Click/Mercatus Grocery Shopping Survey is an ongoing independent research initiative created and conducted by Brick Meets Click and sponsored by Mercatus. Brick Meets Click conducted the survey on July 29-30, 2021, with 1,892 adults, 18 years and older, who participated in the household’s grocery shopping. Results were adjusted based on internet usage among U.S. adults to account for the non-response bias associated with online surveys. Responses are geographically representative of the U.S. and weighted by age to reflect the national population of adults, 18 years and older, according to the U.S. Census Bureau. Brick Meets Click used a similar methodology for each of the surveys conducted June 27-28, 2021 (n=1,789), May 28-30, 2021 (n=1,872), Apr. 26-28, 2021 (n=1,941), Mar. 26-28, 2021 (n=1,811), Feb. 26-28, 2021 (n= 1,812), Jan. 28-31, 2021 (n=1,776); throughout 2020, Nov. 11-14 (n=2,067), Aug. 24-26 (n=1,817), Jun. 24-25 (n=1,781), May 20-22 (n=1,724), Apr. 22-24 (n= 1,651), and Mar. 23-25 (n=1,601); and in Aug. 22-24, 2019 (n = 2,485).

About Brick Meets Click

Brick Meets Click is an analytics and strategic insight firm that connects today’s grocery business with tomorrow’s needs. Our clear thinking and practical solutions help clients make their strategies and customer offers more compelling and relevant in the changing U.S. grocery market. We bring deep industry expertise, knowledge of what’s coming next, and fact-based analysis to the challenge of finding new routes to success.

Want more insights like this? Subscribe for full access to Brick Meets Click’s State of the US eGrocery Market Report.

About Mercatus

Mercatus helps leading grocers get back in charge of their eCommerce experience, empowering them to deliver exceptional retailer-branded, end-to-end online shopping, from store to door. Our expansive network of more than 50 integration partners allows grocers to work with their partners of choice, on their terms. Together, we enable clients to create authentic digital shopping experiences with solutions to drive shopper engagement, grow share of wallet and profitability, and quickly adapt to changes in consumer behavior. The Mercatus Integrated Commerce® platform is used by leading North American retailers, including Weis Markets, Save Mart brands, Brookshire’s Grocery Company brands, WinCo Foods, Smart & Final, Stater Bros. Markets and others. Mercatus is headquartered in Toronto, Canada.

Media Contacts

416-603-3406

[email protected]